Starting your savings journey doesn’t require thousands of dollars. Whether you’re setting aside your first emergency fund or building a habit of saving, finding the right account for smaller deposits can make a real difference in your financial growth.

Why Small Savers Often Get Overlooked

Traditional banks have long catered to customers with hefty balances, offering their best rates and perks to those who can maintain thousands in their accounts. Meanwhile, someone trying to save their first $500 faces minimum balance requirements, monthly fees, and interest rates so low they might as well keep their money under the mattress.

The good news? The banking landscape has shifted dramatically. Online banks and credit unions now compete fiercely for every customer, regardless of balance size. They’ve eliminated many barriers that once kept small savers from earning competitive returns.

When you’re working with $100 to $500, every basis point matters. A difference of just 2% APY might seem insignificant, but over time, it determines whether your money actually grows or merely sits there. Consider this: $300 earning 0.01% APY (typical at major brick-and-mortar banks) generates three cents annually. That same $300 at 4.5% APY earns $13.50 — enough for a lunch or a month of a streaming service.

Understanding APY and How It Works With Smaller Balances

Annual Percentage Yield represents your actual earnings after compound interest works its magic. Unlike simple interest, compound interest pays you interest on your interest, creating a snowball effect even with modest amounts.

Here’s what happens with $200 at different rates over one year:

- At 0.01% APY: $200.02

- At 2.00% APY: $204.00

- At 4.50% APY: $209.00

The difference becomes more pronounced as you continue adding to your account. If you deposit just $50 monthly to that initial $200, after one year at 4.5% APY, you’d have approximately $827, compared to $800 at 0.01% APY. That extra $27 came from doing nothing more than choosing the right account.

The Power of Consistency Over Size

Many people hesitate to open a high-yield account because they feel their deposits are too small to matter. This mindset costs money. Banks calculate interest daily, meaning even if you start with $100 and add $25 here and there, you’re earning returns from day one.

Top Accounts That Welcome Small Deposits

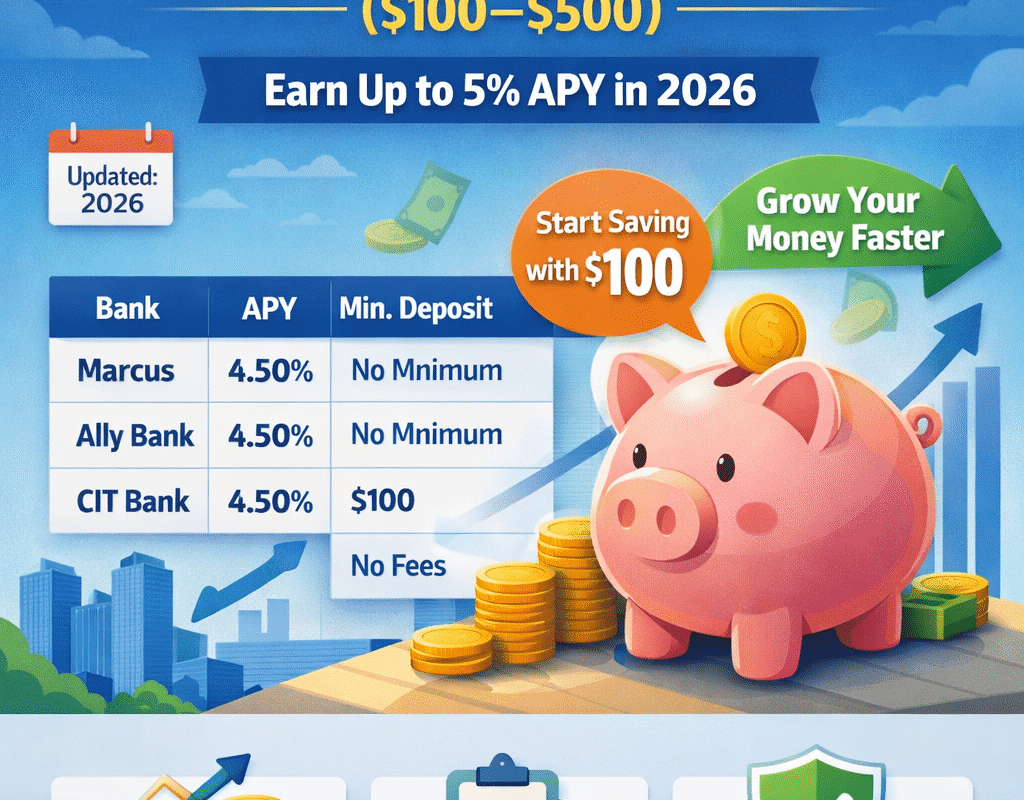

Marcus by Goldman Sachs

Marcus stands out for its straightforward approach. No minimum deposit, no monthly fees, and consistently competitive rates make it ideal for beginning savers. The interface feels refreshingly simple — no upselling, no confusing fee structures, just your money earning interest.

What sets Marcus apart for small depositors is their savings calculator tool. You can input your starting amount (even $1) and planned monthly contributions to see projected growth. This transparency helps new savers visualize their progress and stay motivated.

The mobile app deserves mention too. While some online banks feel clunky on mobile devices, Marcus provides a smooth experience whether you’re checking your balance or transferring funds. Transfers from external accounts typically complete within 2-3 business days.

Ally Bank Online Savings

Ally revolutionized online banking by treating all customers equally, regardless of balance. Their savings account requires no minimum deposit and maintains competitive rates across all balance tiers. This means someone with $150 gets the same APY as someone with $15,000.

Beyond the numbers, Ally excels at customer education. Their website features genuinely helpful articles about saving strategies, not just promotional content. They also offer a unique bucket feature, allowing you to organize your savings into different goals within one account — perfect for visualizing progress on multiple small savings targets.

Customer service at Ally operates 24/7, including live chat. When you’re new to online banking or high-yield accounts, having accessible support matters. Representatives can walk you through setting up automatic transfers or explain how interest compounds on your balance.

CIT Bank Platinum Savings

CIT Bank takes an interesting approach with their Platinum Savings account. While they require a $100 minimum deposit, they offer one of the highest APYs available without requiring massive balances or monthly deposits. Once you’ve opened the account with $100, you can maintain any balance without fees.

Their interest rate structure remains competitive across all balances, though they do offer slightly higher rates if you maintain $5,000 or more. For those starting small but planning to grow their savings, this provides an incentive without penalizing current balances.

CIT’s website might feel less polished than some competitors, but the fundamentals work well. Account opening takes about 10 minutes online, and their security measures include two-factor authentication and encryption that meets federal standards.

American Express Personal Savings

American Express, known primarily for credit cards, offers a compelling savings option with no minimum balance requirement and no monthly fees. Their rates consistently rank among the highest available, and the backing of a established financial institution provides peace of mind.

The account links easily with American Express credit cards if you have them, but works perfectly fine as a standalone product. One minor limitation: you can only link one external bank account for transfers. This might frustrate those who maintain accounts at multiple institutions, though most savers with smaller balances won’t find this restrictive.

Customer reviews frequently praise the reliability of their platform and the speed of transfers. While they don’t offer a checking account, making this a savings-only relationship, the simplicity appeals to those who want their high-yield savings separate from daily spending.

Credit Union Options Worth Considering

Alliant Credit Union High-Rate Savings

Credit unions operate differently than banks, returning profits to members through better rates and lower fees. Alliant Credit Union exemplifies this model, offering exceptional rates with just a $5 minimum deposit (technically your membership share).

Joining Alliant requires membership eligibility, but they make this easy. You can qualify by making a $10 donation to Alliant Credit Union Foundation, essentially a one-time $10 fee for lifetime access to their products. Considering the rate advantage often exceeds 0.5% over traditional banks, you’ll recoup that donation quickly.

Alliant provides both online and mobile banking that rivals any digital bank. Their customer service, consistently rated highly, operates through U.S.-based call centers. They also offer a checking account with competitive features, making them suitable for those wanting their primary banking relationship with one institution.

Consumers Credit Union

Consumers Credit Union rewards relationship depth rather than balance size. Their basic savings account offers competitive rates, but members who use multiple products (checking, credit card, loans) can earn bonus rates that push their APY even higher.

The membership requirement involves a $5 donation to the Consumers Cooperative Association, similar to Alliant’s model. Once you’re in, you gain access to their full suite of products. Their rewards checking account deserves particular attention, offering cash back on debit card purchases — unusual for checking accounts.

For savers starting with $100-$500, the ability to earn extra through account relationships rather than balance requirements presents an alternative path to maximizing returns.

Digital-First Banks Changing the Game

Varo Savings Account

Varo operates exclusively through mobile devices, eliminating overhead costs and passing savings to customers. Their standard savings rate matches or beats most competitors, but their automatic savings features particularly benefit those building initial deposits.

The Save Your Change feature rounds up debit card purchases and transfers the difference to savings. Spend $3.75 on coffee, and $0.25 automatically moves to savings. These micro-deposits add up surprisingly fast, often adding $20-30 monthly without conscious effort.

Varo also offers a unique high-yield option: meet simple requirements like receiving $1,000+ in direct deposits and making 5 debit card purchases monthly, and your savings APY increases substantially on balances up to $5,000. This rewards account activity rather than balance size, perfect for active savers with smaller amounts.

Chime Savings Account

Chime targets younger savers who might be opening their first high-yield account. While their base savings rate isn’t the highest, their automatic savings features help grow small balances quickly.

The Save When You Get Paid feature automatically transfers a percentage of direct deposits to savings. Set it to 10%, and $30 of a $300 deposit moves to savings instantly. Combined with their round-up feature, users often report saving more than they expected without feeling the pinch.

Chime’s early direct deposit feature (up to two days early) also helps with saving momentum. Getting paid on Wednesday instead of Friday means two extra days of interest accumulation, plus the psychological benefit of seeing progress sooner.

Maximizing Returns on Limited Funds

The Art of Rate Chasing vs. Stability

Some savers constantly move money to chase the highest rates, while others pick one good account and stick with it. With smaller balances, the math often favors stability. Moving $300 to gain an extra 0.25% APY earns you an additional $0.75 annually — hardly worth the effort and potential transfer delays.

Instead, focus on finding an account with consistently competitive rates from an institution you trust. Look at rate history rather than just current offers. Some banks attract deposits with high introductory rates, then drop them significantly. Others maintain steady, competitive rates that might be 0.1% lower but remain reliable.

Automatic Transfers: Your Secret Weapon

The most effective strategy for growing small deposits involves automatic transfers. Schedule $25 or $50 to move from checking to savings right after each payday. You’ll adjust to the slightly lower checking balance quickly, while your savings grow without requiring willpower or memory.

Many successful savers use the “pay yourself first” principle. Before paying bills or discretionary spending, move money to savings. Even $10 per week becomes $520 annually, plus interest. Starting small and increasing gradually often works better than attempting large, unsustainable transfers.

Using Windfalls Wisely

Tax refunds, birthday gifts, and side gig earnings provide opportunities to boost your savings significantly. Instead of viewing these as “extra” money for spending, consider them savings accelerators. A $300 tax refund deposited in April grows to $311 by year-end at 4.5% APY, and that’s before adding regular contributions.

Common Mistakes to Avoid

Ignoring Account Fees

Monthly maintenance fees devastate small balances. A $5 monthly fee on a $200 balance equals 30% annually — no interest rate can overcome that. Always verify fee structures before opening accounts, and understand any requirements for fee waivers.

Some accounts waive fees with direct deposit or minimum balances. Others charge for excessive transactions (federal regulations limit certain withdrawals to six monthly). Paper statement fees, ATM fees, and transfer fees can also erode returns. Choose accounts with truly free structures for small balances.

Forgetting About Taxes

Interest earned on savings accounts is taxable income. While someone earning $10 in annual interest won’t owe much, it’s still reportable on tax returns. Banks issue 1099-INT forms for interest exceeding $10 annually. Factor taxes into your calculations when comparing returns, though at current tax rates, the impact on small balances remains minimal.

Overlooking Account Insurance

Ensure your chosen institution provides FDIC insurance (banks) or NCUA insurance (credit unions). This protection covers up to $250,000 per depositor, per institution, per ownership category. While your $100-$500 falls well within limits, some online-only institutions might use partnership structures that complicate coverage. Verify insurance directly through FDIC or NCUA websites, not just the bank’s claims.

Building Your Savings Strategy

Starting With Your First $100

Opening your first high-yield savings account with $100 marks an important financial milestone. Choose an institution based on your comfort level with technology, need for customer support, and long-term goals. If you’re tech-savvy and comfortable with mobile-only banking, options like Varo or Chime might appeal. If you prefer established names with robust customer service, Marcus or Ally make sense.

Once opened, focus on consistency over amount. Adding $20 monthly beats sporadic $100 deposits for building habits and seeing steady progress. Watch your balance grow for a few months — the psychological boost from seeing interest credited monthly reinforces positive behavior.

Growing From $100 to $500

The journey from $100 to $500 teaches valuable lessons about money management. You’ll discover which automatic savings methods work for your lifestyle. You might find that daily coffee savings challenges don’t suit you, but automatic transfers thrive. Or perhaps round-up features accumulate faster than expected.

During this growth phase, resist the temptation to withdraw funds for non-emergencies. The satisfaction of reaching $500 provides momentum for larger goals. Many savers report that their first $500 felt harder to save than their second $5,000 — the habits you build matter more than the amounts.

Planning Beyond $500

Once you’ve successfully saved $500, reassess your account choice. Some accounts offer better rates at higher balances, while others maintain flat rates regardless. You might also consider dividing funds between different goals — keeping emergency savings separate from vacation or purchase funds.

Don’t rush to invest these initial savings in riskier assets. A solid high-yield savings foundation provides security and liquidity that investments can’t match. Many financial advisors recommend maintaining 3-6 months of expenses in safe, accessible accounts before pursuing investment returns.

Frequently Asked Questions

How quickly can I open an online savings account?

Most online applications take 10-15 minutes. Approval might be instant or take 1-2 business days. Initial funding via electronic transfer usually completes within 2-3 business days, though some banks offer instant funding through debit cards for smaller amounts.

Can I have multiple high-yield savings accounts?

Absolutely. Many savers maintain accounts at different institutions for various goals. Just track your total interest earned for tax purposes and ensure you’re meeting any minimum balance requirements to avoid fees.

Will opening a savings account affect my credit score?

Most savings accounts don’t require credit checks, so they won’t impact your score. Some banks perform soft inquiries that don’t affect credit. If you’re denied an account, it’s usually due to banking history (ChexSystems) rather than credit issues.

What happens if the bank lowers interest rates?

Banks can adjust rates anytime for variable-rate accounts. Your principal remains safe, but earnings decrease. Monitor rate changes and be prepared to switch if your bank consistently lags competitors, though avoid excessive switching for minimal differences.

Is it safe to bank with online-only institutions?

FDIC-insured online banks offer the same protection as traditional banks. Many use advanced security measures like encryption, two-factor authentication, and fraud monitoring. Research any institution through FDIC.gov before opening accounts.

Should I save or pay off debt first?

Financial experts recommend saving at least $500-$1,000 for emergencies even while paying debt. This prevents using credit cards for unexpected expenses. High-interest debt (above 20% APR) should take priority after establishing minimal emergency savings.

Moving Forward With Confidence

Building savings with modest amounts requires choosing the right account and developing consistent habits. The institutions mentioned here remove traditional barriers, offering competitive returns without demanding large balances or charging punitive fees.

Remember that everyone starts somewhere. Today’s $100 deposit could grow into tomorrow’s financial security through compound interest and regular contributions. The key lies not in the starting amount but in taking action and maintaining momentum.

Select an account that aligns with your needs, set up automatic transfers you can maintain, and watch your money grow. Small deposits in the right high-yield savings account beat large amounts sitting in traditional accounts earning nothing. Your future self will thank you for starting today, regardless of the amount.