Explore advanced risk transfer mechanisms in insurance, including securitization, derivatives, and reinsurance. Learn how these innovative strategies reduce exposure, improve capital efficiency, and shape the future of risk management.

Why Risk Transfer Is the Lifeline of Insurance

Insurance is fundamentally about transferring risk. Individuals and organizations purchase policies to protect themselves against unpredictable losses, while insurers use various strategies to spread and manage those risks. Traditionally, risk transfer was limited to reinsurance agreements and diversification across policyholders. However, in today’s interconnected global economy, insurers face increasingly complex, high-impact, and systemic risks that require more sophisticated tools.

This is where advanced risk transfer mechanisms come into play. These innovative solutions—ranging from securitization and catastrophe bonds to insurance-linked derivatives and alternative risk financing—enable insurers to mitigate exposure, protect balance sheets, and unlock new opportunities for capital optimization.

In this article, we’ll take a deep dive into the mechanisms, benefits, challenges, and future trends shaping the world of advanced risk transfer in the insurance sector.

Understanding the Concept of Risk Transfer in Insurance

Risk transfer occurs when an insurer shifts part of its liability to another entity, usually in exchange for a premium or financial compensation. The objective is to spread potential losses and ensure the insurer’s financial stability.

- Primary Insurance: The policyholder transfers risk to the insurer.

- Reinsurance: The insurer further transfers part of its risk to another insurance company.

- Alternative Risk Transfer (ART): Non-traditional strategies that involve capital markets, securitization, or hybrid financial products.

As risks grow in frequency, severity, and unpredictability—driven by climate change, cyberattacks, and global economic volatility—conventional reinsurance is no longer sufficient. Hence the rise of advanced mechanisms.

Traditional vs. Advanced Risk Transfer

- Traditional Methods: Mainly involve proportional and non-proportional reinsurance. While effective, they often concentrate risk within the insurance industry itself.

- Advanced Methods: Incorporate financial markets, structured products, and innovative financial engineering, allowing risks to be transferred to a broader investor base.

This shift opens the door to global capital markets—a pool far larger than the insurance industry alone.

Key Advanced Risk Transfer Mechanisms

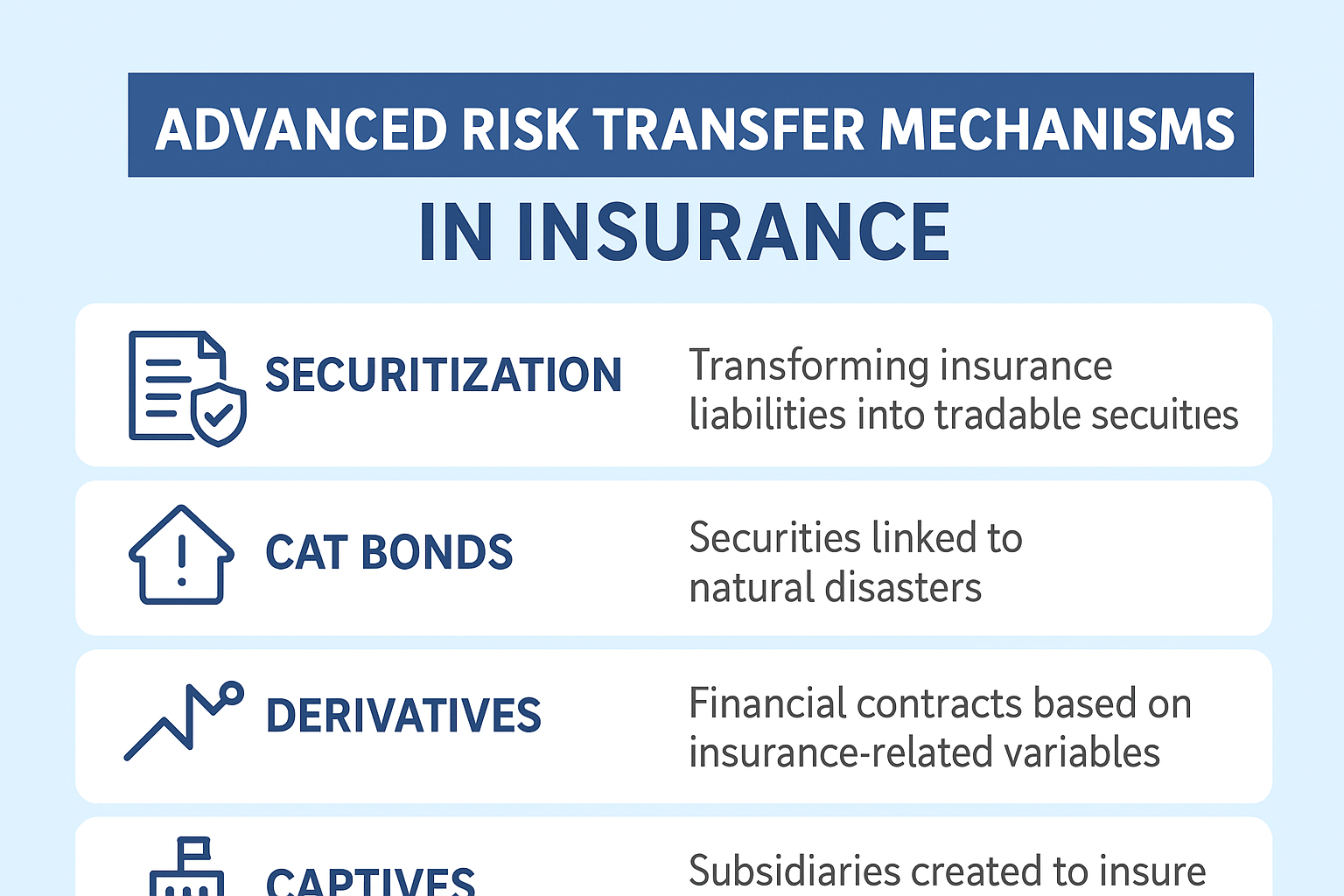

1. Securitization of Insurance Risks

Insurance securitization involves transforming insurance liabilities into tradable securities. Investors buy these securities, effectively taking on a share of the risk in exchange for potential returns.

Examples:

- Catastrophe Bonds (Cat Bonds): Securities linked to natural disasters such as hurricanes or earthquakes. If the catastrophe occurs, investors lose some or all of their principal, which is used to cover insurer losses.

- Mortality Bonds: Securities tied to life expectancy or mortality rates.

Benefits:

- Provides insurers with access to capital markets.

- Reduces dependence on traditional reinsurers.

- Enhances diversification of risk.

2. Insurance Derivatives

Insurance derivatives are financial contracts whose value depends on insurance-related variables, such as claim frequencies, mortality rates, or catastrophe indices.

- Weather Derivatives: Used by energy companies, agriculture firms, and insurers to hedge against climate variability.

- Catastrophe Futures: Traded on exchanges, these futures allow participants to speculate on or hedge against disaster-related losses.

Advantage:

They offer liquidity, flexibility, and transparency in transferring risk.

3. Collateralized Reinsurance

This mechanism involves fully collateralized structures, where investors set aside funds in a trust to cover potential claims. It minimizes counterparty credit risk, making it a safer option compared to traditional reinsurance.

4. Alternative Risk Financing (ARF)

Alternative risk financing includes techniques like captive insurance, finite risk reinsurance, and multi-year, multi-line covers.

- Captive Insurance: A subsidiary formed by a parent company to insure its own risks.

- Finite Risk Reinsurance: Combines risk transfer with financing, spreading risk and cost over time.

5. Catastrophe Bonds (Detailed Spotlight)

Among all advanced mechanisms, catastrophe bonds (cat bonds) have gained significant popularity. They act as a bridge between insurers and global investors, channeling massive amounts of capital into risk absorption.

- Structure: Investors purchase bonds, receive attractive coupon payments, but risk losing their principal if a triggering event occurs.

- Market Growth: The cat bond market has grown significantly, surpassing billions in outstanding issuance globally.

Benefits of Advanced Risk Transfer Mechanisms

- Capital Efficiency: Frees up insurers’ balance sheets, enabling them to write more policies.

- Diversification: Transfers risks beyond the insurance industry into global capital markets.

- Resilience: Provides additional financial security against catastrophic events.

- Investor Opportunities: Offers investors uncorrelated assets with attractive returns.

- Innovation: Encourages new product development and hybrid financing models.

Challenges and Limitations

- Complexity: Structures are often complicated, requiring specialized knowledge.

- Liquidity Issues: Some products, like cat bonds, may not have deep secondary markets.

- Regulatory Barriers: Different jurisdictions have varying laws on securitization and derivatives.

- Model Risk: Dependence on catastrophe models, which may not accurately predict real-world losses.

- Investor Hesitancy: Some investors remain cautious about insurance-linked securities due to uncertainty.

The Role of Technology in Enhancing Risk Transfer

Emerging technologies are reshaping advanced risk transfer strategies:

- Big Data Analytics: Improves risk modeling and loss prediction accuracy.

- Artificial Intelligence (AI): Enhances pricing and claims analysis.

- Blockchain: Ensures transparency, traceability, and faster settlements in insurance-linked securities.

- Parametric Insurance Models: Trigger payouts automatically when measurable parameters (e.g., rainfall levels, wind speed) are met.

Case Studies

Hurricane Katrina and Cat Bonds

The devastation of Hurricane Katrina highlighted the importance of catastrophe bonds, which provided insurers with additional liquidity to handle unprecedented claims.

Weather Derivatives in Agriculture

Farmers use weather derivatives to hedge against droughts or excessive rainfall, ensuring stable income despite climatic uncertainties.

Future Trends in Advanced Risk Transfer

- Integration with Climate Finance: Insurers and governments leveraging cat bonds to fund disaster relief.

- Expansion into Emerging Markets: Microinsurance linked to risk transfer products in developing countries.

- Green Bonds and ESG-Linked Insurance Securities: Aligning insurance-linked securities with sustainability goals.

- AI-Driven Risk Forecasting: Machine learning models predicting extreme weather with greater accuracy.

- Hybrid Structures: Combining reinsurance, securitization, and parametric triggers for maximum efficiency.

Ethical and Regulatory Considerations

- Fairness and Accessibility: Ensuring that advanced mechanisms do not leave vulnerable populations uninsured.

- Global Coordination: Developing harmonized international standards for securitization and derivatives.

- Transparency: Simplifying communication with investors and regulators about complex products.

Conclusion: A New Era for Insurance Risk Management

Advanced risk transfer mechanisms represent a paradigm shift in how insurers manage uncertainty. By tapping into capital markets, embracing securitization, and leveraging technology, the insurance industry has built new pathways for resilience against catastrophic and systemic risks.

However, with innovation comes responsibility. The challenge lies in ensuring that these mechanisms are transparent, fair, and sustainable, while meeting the demands of both insurers and investors.

The future of insurance will be defined not only by how risks are priced but by how effectively they are transferred, diversified, and shared across global financial ecosystems.